Owning a home in a high-risk area comes with unique challenges and responsibilities, especially when it comes to securing adequate homeowners insurance.

High-risk areas, often prone to natural disasters like floods, hurricanes, wildfires, and earthquakes, require specialized insurance coverage to protect homeowners from significant financial losses. This article delves into the intricacies of homeowners insurance for high-risk areas, exploring the types of coverage available, the factors affecting insurance costs, and tips for obtaining the best policy.

Understanding High-Risk Areas

High-risk areas are regions more susceptible to natural disasters and severe weather events. These areas might face frequent threats from hurricanes, tornadoes, floods, wildfires, or earthquakes. Insurance companies classify these regions based on historical data, climate patterns, and the likelihood of future incidents. As a result, homeowners in these areas often face higher insurance premiums and may need to purchase additional coverage to fully protect their properties.

Types of Coverage for High-Risk Areas

1. Standard Homeowners Insurance

Standard homeowners insurance policies provide coverage for common perils such as fire, theft, and certain types of water damage. However, they often exclude or limit coverage for natural disasters prevalent in high-risk areas. Therefore, additional policies or endorsements are usually necessary.

2. Flood Insurance

Flood insurance is essential for homes in flood-prone areas. Standard homeowners insurance typically does not cover flood damage, so a separate flood insurance policy, often through the National Flood Insurance Program (NFIP), is required. Flood insurance covers the structure of the home and its contents against flood-related damage.

Best Life Insurance Policies for Families: Securing Your Loved Ones’ Future

Affordable health insurance plans

3. Windstorm and Hurricane Insurance

In hurricane-prone regions, windstorm and hurricane insurance policies cover damage caused by high winds, including damage to roofs, windows, and other parts of the home. Some states have specialized windstorm insurance pools for high-risk areas where private insurers may not provide coverage.

4. Earthquake Insurance

Homeowners in earthquake-prone areas, such as California, need earthquake insurance, which is usually not included in standard policies. Earthquake insurance covers damage to the structure, personal property, and additional living expenses if the home becomes uninhabitable after an earthquake.

5. Wildfire Insurance

For homes in wildfire-prone areas, wildfire insurance is crucial. While standard policies often cover fire damage, homeowners in high-risk areas may need to pay higher premiums or secure additional coverage specifically for wildfires.

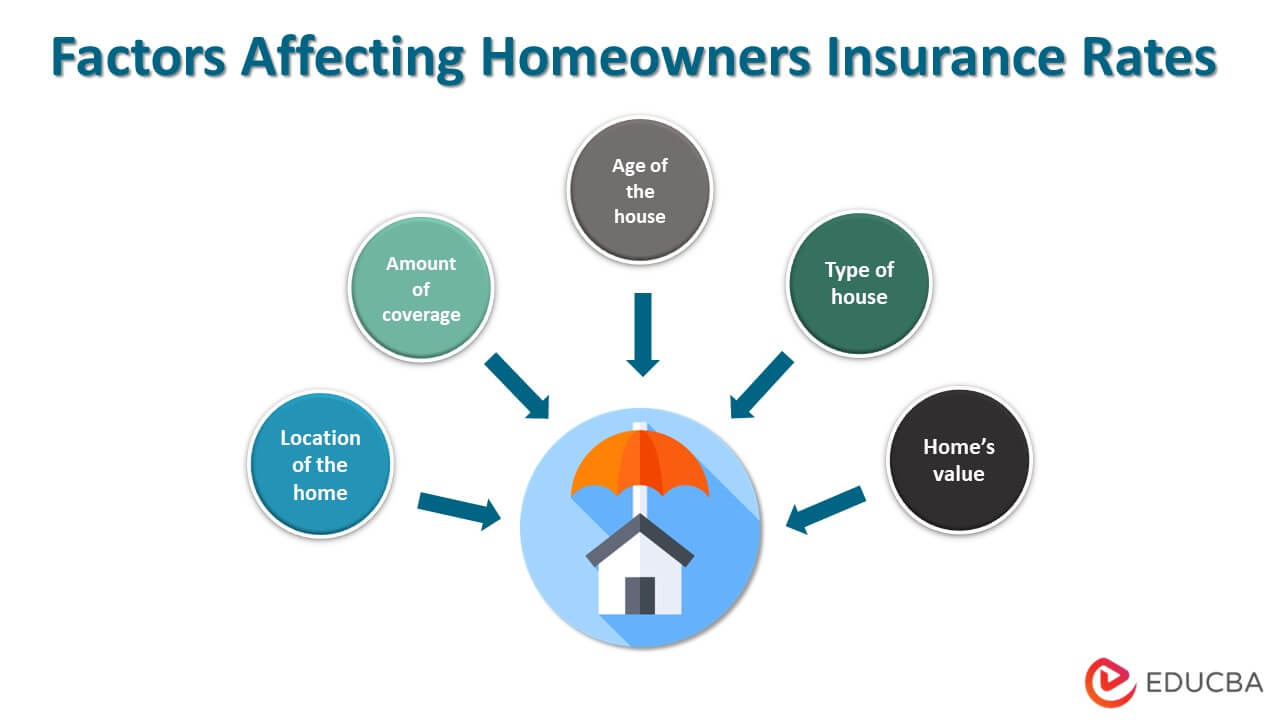

Factors Affecting Homeowners Insurance Costs in High-Risk Areas

1. Location

The location of your home is the most significant factor in determining insurance costs. Areas with a high frequency of natural disasters will generally have higher premiums due to the increased risk.

2. Construction and Materials

The materials and construction methods used in your home can impact insurance costs. Homes built with fire-resistant materials or designed to withstand earthquakes may qualify for lower premiums.

3. Home Value and Replacement Cost

The value of your home and the cost to rebuild it also influence insurance premiums. Higher-value homes and those with more expensive replacement costs will have higher insurance rates.

4. Deductibles

Choosing a higher deductible can lower your insurance premiums. However, this means you will pay more out of pocket in the event of a claim.

5. Mitigation Measures

Implementing risk mitigation measures, such as installing storm shutters, reinforcing roofs, or creating defensible space around your property, can help reduce insurance costs. Many insurers offer discounts for homes with these protective features.

6. Claims History

Your claims history, as well as the claims history of your area, can affect your premiums. Areas with a high number of claims will generally have higher insurance costs.

Comprehensive Auto Insurance Coverage: Everything You Need to Know

Tips for Obtaining Homeowners Insurance in High-Risk Areas

1. Shop Around

Insurance rates can vary significantly between providers, so it’s essential to shop around and compare quotes from multiple insurers. Look for companies that specialize in high-risk areas and have a strong financial rating.

2. Bundle Policies

Consider bundling your homeowners insurance with other policies, such as auto or life insurance, to receive discounts. Many insurers offer multi-policy discounts that can help lower your overall premiums.

3. Assess Coverage Needs

Evaluate your specific coverage needs based on the risks in your area. Ensure that your policy covers the full replacement cost of your home and includes sufficient coverage for personal belongings and additional living expenses.

4. Review Policy Exclusions

Carefully review the exclusions in your policy to understand what is not covered. This will help you identify any additional policies or endorsements you may need.

5. Invest in Mitigation Measures

Investing in home improvements that reduce risk can help lower your insurance premiums. Discuss with your insurance provider which mitigation measures qualify for discounts and implement them to enhance your home’s safety.

6. Maintain Good Credit

Maintaining a good credit score can positively impact your insurance premiums. Insurers often consider credit scores when determining rates, so keeping your credit in good standing can help reduce costs.

7. Seek Professional Advice

Consult with an insurance agent or broker who specializes in high-risk areas. They can provide valuable insights, help you navigate the complexities of homeowners insurance, and recommend the best coverage options for your situation.

Conclusion

Securing homeowners insurance for high-risk areas requires careful consideration and planning. Understanding the types of coverage available, the factors affecting insurance costs, and implementing risk mitigation measures can help you obtain the best policy for your needs. By taking these steps, you can protect your home and financial future against the unique risks associated with high-risk areas, ensuring peace of mind and security for you and your family.

Renters Insurance for College Students: Protecting Your Belongings and Peace of Mind

Homeowners Insurance for High-Risk Areas: What You Need to Know

Best Life Insurance Policies for Families: Securing Your Loved Ones’ Future